WHAT YOU'LL LEARN IN THIS MODULE

- → The exact difference between income, savings, and wealth — and why confusing them keeps most people broke

- → Why a ₹2 lakh/month earner can have less wealth than a ₹50,000/month earner

- → The one number that actually measures your financial health (it's not your salary)

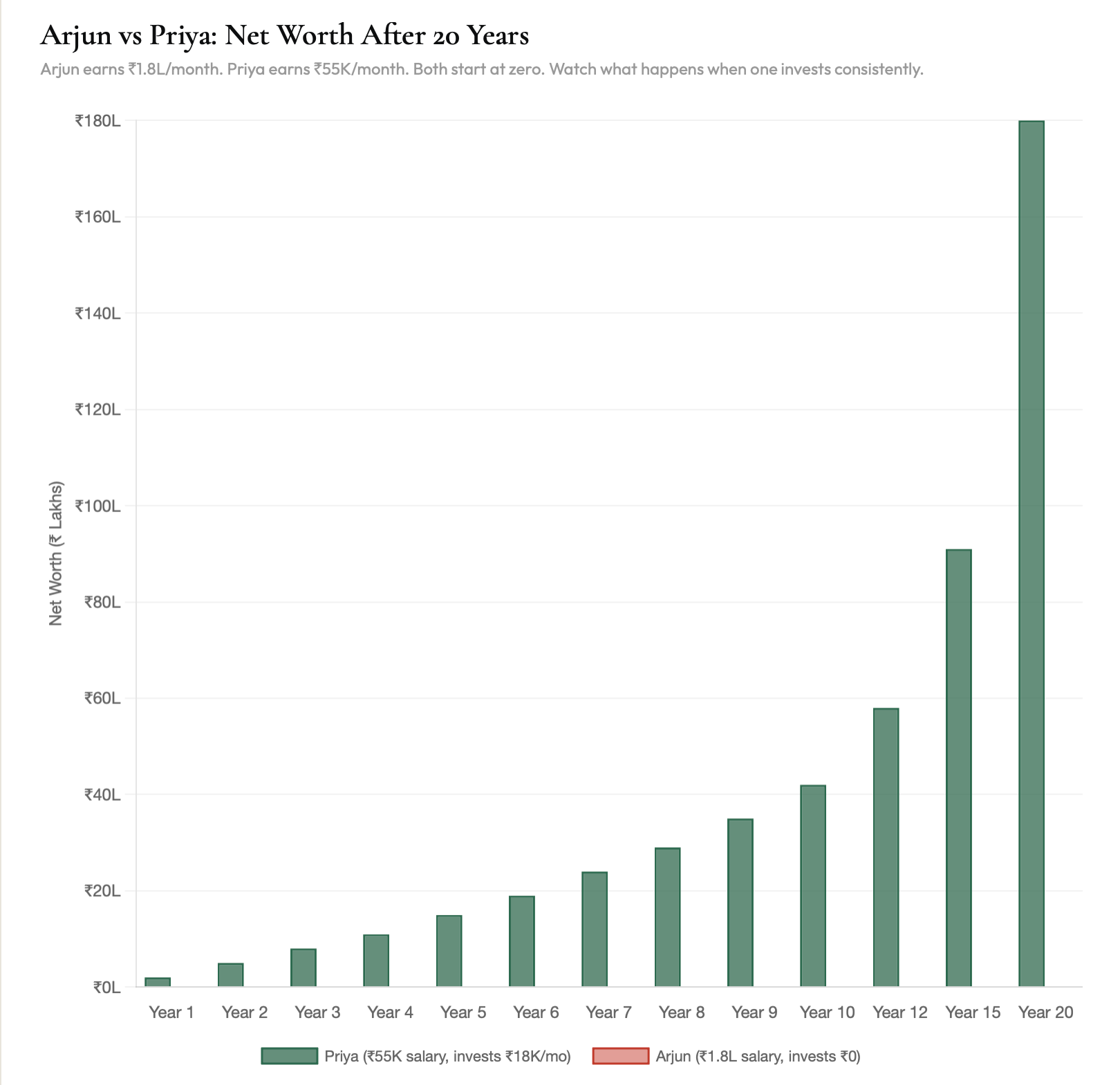

Meet Arjun. He earns ₹1.8 lakh per month at a Bangalore tech firm. He drives a new Honda City, holidays in Bali every year, and lives in a 2BHK in Koramangala. By every social measure, Arjun is doing well.

Now meet Priya. She earns ₹55,000 per month as a teacher in Pune. She takes the bus, cooks at home, and hasn't upgraded her phone in three years.

Priya has significantly more wealth than Arjun.

Arjun spends ₹1.75 lakh every month. His car loan, rent, lifestyle expenses, and EMIs leave him with almost nothing at month-end. His net worth — what he would have if he sold everything and paid every debt — is close to zero, possibly negative.

Priya invests ₹18,000 every month, has been doing so for 6 years, and has quietly built a corpus of over ₹18 lakhs . She owns her future. Arjun owns his lifestyle.

This is the foundational truth of personal finance that almost nobody teaches you.

Income, Savings, and Wealth: Three Different Things

Most people treat these three words as roughly the same thing. They aren't. Understanding the difference between them is the first — and most important — mental shift in your financial life.

| Term | What It Means | Example | Does It Build Wealth? |

|---|---|---|---|

| Income | Money that flows IN — salary, freelance, business revenue | ₹1.8L/month salary | Only if you keep it |

| Savings | Income minus expenses — what's left over | ₹5,000 left at month-end | Only if you invest it |

| Wealth | The total value of assets you OWN minus all debts | ₹18L MF + ₹2L savings - ₹0 debt = ₹20L net worth | Yes — this is the actual goal |

Income is a flow. Wealth is a stock. You can have a very high income and zero wealth — that's Arjun. You can have modest income and real wealth — that's Priya. The path from one to the other has a name: the savings rate.

The Number That Actually Measures Your Financial Health

Forget your salary. Forget your job title. The single most important financial number you can know right now is your savings rate — the percentage of your income you invest and keep.

Savings Rate vs Years to Financial Freedom

Assuming 10% annual returns. How long until your investments cover your expenses forever.

Look at that curve. Going from a 10% savings rate to a 20% savings rate doesn't just halve your time to financial freedom — it cuts it by almost 15 years. The math is brutally, beautifully clear.

Most Indians save between 5–15% of their income. The people who reach financial freedom before 50 typically save 30–40%. That's the gap. It's not about earning more. It's about keeping more of what you earn.

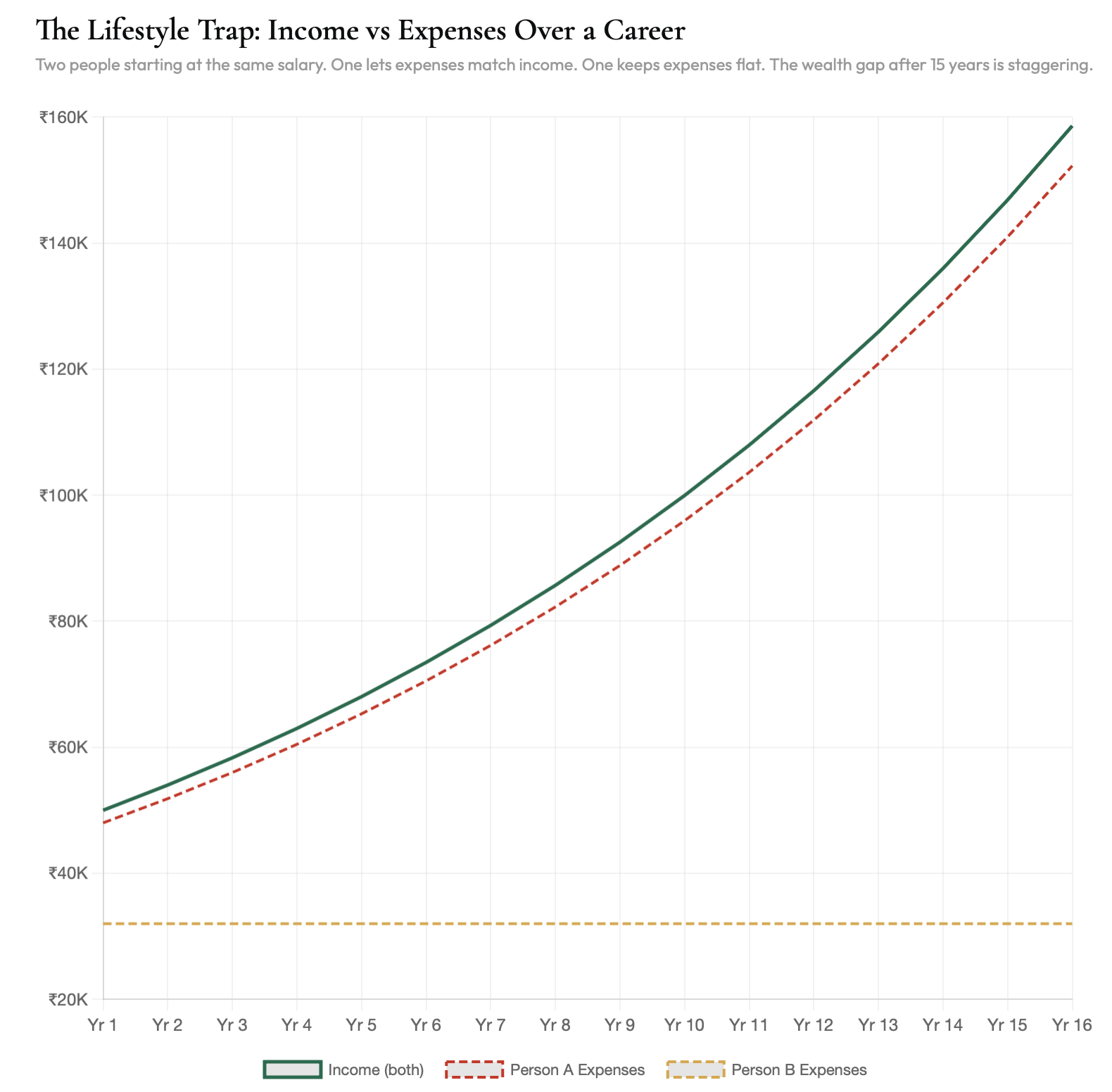

The Lifestyle Trap: Why Earning More Often Helps Less Than You Think

There's a cruel paradox hiding in salary hikes. When your income goes up, your lifestyle almost always goes up with it — often faster. This is called lifestyle inflation , and it is the single biggest wealth-destroyer in the Indian middle class.

You get a ₹30,000 raise. Suddenly, a better car feels appropriate. Dining out more often makes sense. That weekend trip to Goa is now within reach. By the time the credit card statement arrives, your ₹30,000 raise has completely disappeared into a higher lifestyle — and your savings rate hasn't moved.

The fastest way to build wealth is not to earn more. It's to let your lifestyle grow slower than your income.

The green area in that chart — the gap between income and expenses — is your wealth. Notice how Person A's gap stays the same even as income rises. Notice how Person B's gap grows every single year. At year 15, they earn the same salary. But one has built a fortune and the other has built a lifestyle.

Assets vs Liabilities: What Rich People Actually Buy

Robert Kiyosaki wrote about this in Rich Dad Poor Dad , but the Indian context makes it even more stark. Most people spend their working years buying liabilities — things that take money out of their pocket every month. The wealthy spend their early years buying assets — things that put money into their pocket.

|

LIABILITIES — MONEY LEAVES YOU |

ASSETS — MONEY COMES TO YOU |

|

What Most People Buy |

What Wealthy People Buy First |

|

|

Your Wealth Number: Calculate It Right Now

Here is a simple exercise. Open a notes app. Write these two columns:

Assets (what you own): Mutual fund balance + bank FDs + PPF + gold value + any property equity (market value minus outstanding loan)

Liabilities (what you owe): Home loan outstanding + car loan + personal loan + credit card balance + any other debt

Subtract liabilities from assets. That number is your net worth — your actual wealth today. If it's negative, don't panic. The fact that you're reading this means you're about to change it. If it's positive, your only job now is to grow it systematically every single month.

A good benchmark: by age 30, aim for a net worth of at least 1× your annual salary. By 40, aim for 5×. By 50, aim for 15×. These are not rules — they're useful landmarks to see where you stand on the journey.

Stop measuring your financial health by your salary package. Your net worth is the only number that matters. The fastest path to building it is ruthlessly simple: spend less than you earn, invest the difference automatically, and never let your lifestyle inflate faster than your savings rate. Priya doesn't earn more than Arjun. She just keeps more — and that changes everything.

All content is for educational purposes only. Not SEBI-registered financial advice.

3 Things to Do Today

Take action on what you just learned — right now, before you forget

Calculate your actual net worth

Open your banking apps right now. Add up everything you own (savings, FDs, mutual funds, gold). Subtract everything you owe (loans, credit card). Write that number down. That's your starting line.

Calculate your savings rate this month

Take your monthly income. Subtract all expenses. Divide by income. Multiply by 100. If it's below 20%, your next step is clear: find one expense to cut before the month ends — even ₹500 counts.

Set up an auto-transfer on salary day

Log into your bank right now and set a standing instruction: on the day your salary arrives, automatically transfer a fixed amount to a separate savings account. Even ₹2,000. Pay yourself before lifestyle gets it.