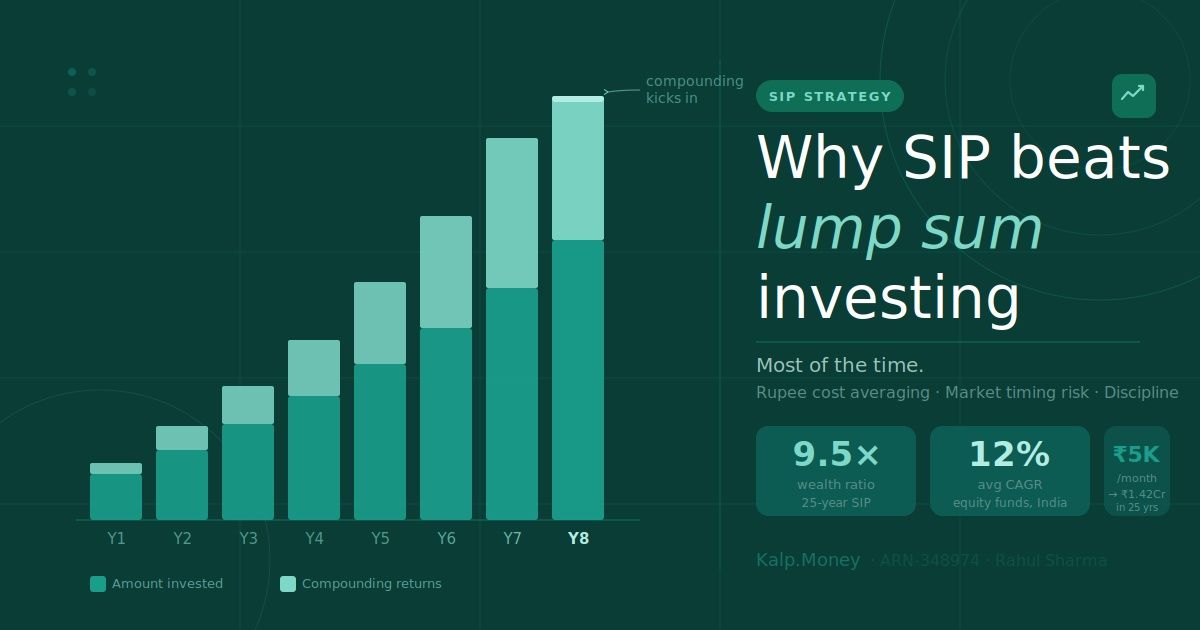

The core idea: Rupee Cost Averaging

When you invest a fixed amount every month regardless of market conditions, you buy more units when prices are low and fewer units when prices are high. Over time, this averages out your cost per unit — a phenomenon called Rupee Cost Averaging (RCA).

It sounds simple. But the psychological and mathematical effects are profound.

💡 A ₹10,000 monthly SIP in the Nifty 50 index over the last 10 years would have turned ₹12 Lakhs invested into over ₹28 Lakhs. That's a CAGR of ~16.4%.

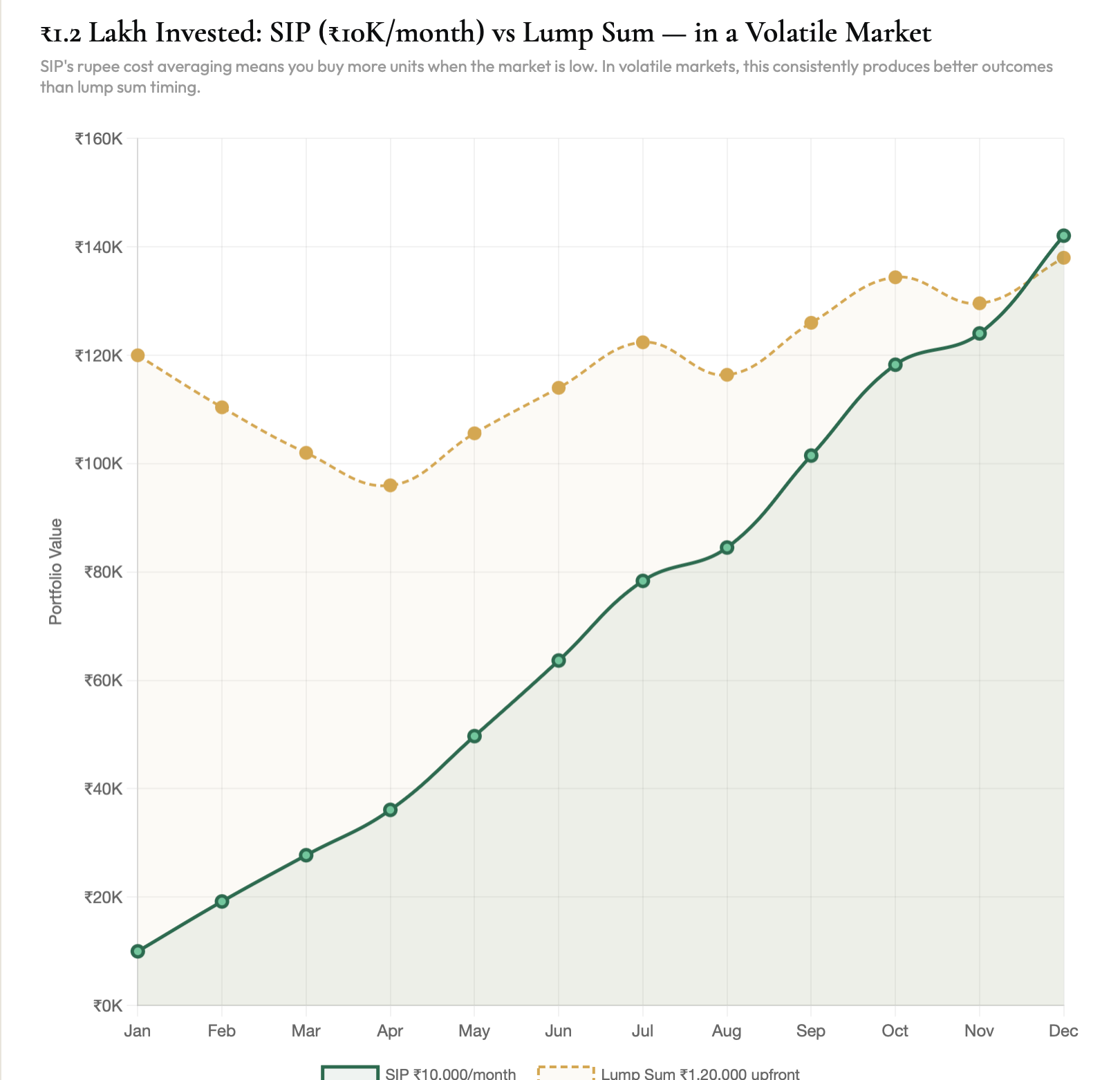

Why SIP wins in volatile markets

Markets don't go up in a straight line. They crash, recover, consolidate, and surge — often unpredictably. A lump sum investor who puts ₹5 Lakhs on the wrong day (say, market peak before a crash) might wait years to recover. An SIP investor? They'd actually benefit from the crash — buying more units at lower prices.

- SIPs remove the need to "time the market"

- Crashes become buying opportunities, not anxiety triggers

- Discipline compounds over years, not just returns

When lump sum wins

If markets have just crashed significantly and you have a large sum ready to deploy, a lump sum investment can outperform — because you're buying at a discount and have more capital compounding from day one. But most investors don't have large sums lying around, and timing markets is notoriously difficult even for professionals.

🎯 The practical answer: SIP for monthly savings. Lump sum for bonuses, windfalls, or when markets have corrected 20%+.

The best SIP strategy

Start as early as possible. Increase your SIP amount every year (step-up SIP). Don't stop during market corrections. Stay invested for at least 7+ years. These four habits, consistently followed, create most of the wealth in long-term SIP portfolios.

For most salaried Indians investing monthly, SIP is the most practical approach. It removes the need to time markets, builds discipline through automation, and benefits from volatility via rupee cost averaging. The only exception is investing a large lump sum during a sharp market correction (20%+), which can outperform phased investing. Otherwise, start your SIP now—the earlier, the better.

All content is for educational purposes only. Not SEBI-registered financial advice.

3 Things to Do Today

From the SIP vs Lump Sum module — act while the insight is fresh

Start your first SIP — even if it's ₹500

Open Zerodha Coin, Groww, or INDmoney. Pick any Nifty 50 index fund. Set up a monthly SIP for the smallest amount you're comfortable with. The amount doesn't matter right now — the habit does. You can increase it any time.

Set your SIP date to salary day + 2

When setting up your SIP, choose a debit date 2 days after your salary credit date. This ensures the money goes to your investment before it can disappear into expenses. Automate this and you'll never need willpower again.

Set a reminder to increase your SIP by 10% in January

Right now, open your phone calendar and set a recurring reminder every January 1st: "Increase all SIPs by 10%." This Step-Up SIP strategy, done consistently, can add 40–60% more to your final corpus compared to a flat SIP. One reminder. Decades of impact.