What Einstein (probably) said

The quote "compound interest is the eighth wonder of the world" is often attributed to Einstein. Whether he said it or not is debated — but the math is indisputable. Compounding is simply earning returns on your returns. It's a mathematical snowball that starts slowly and then accelerates dramatically.

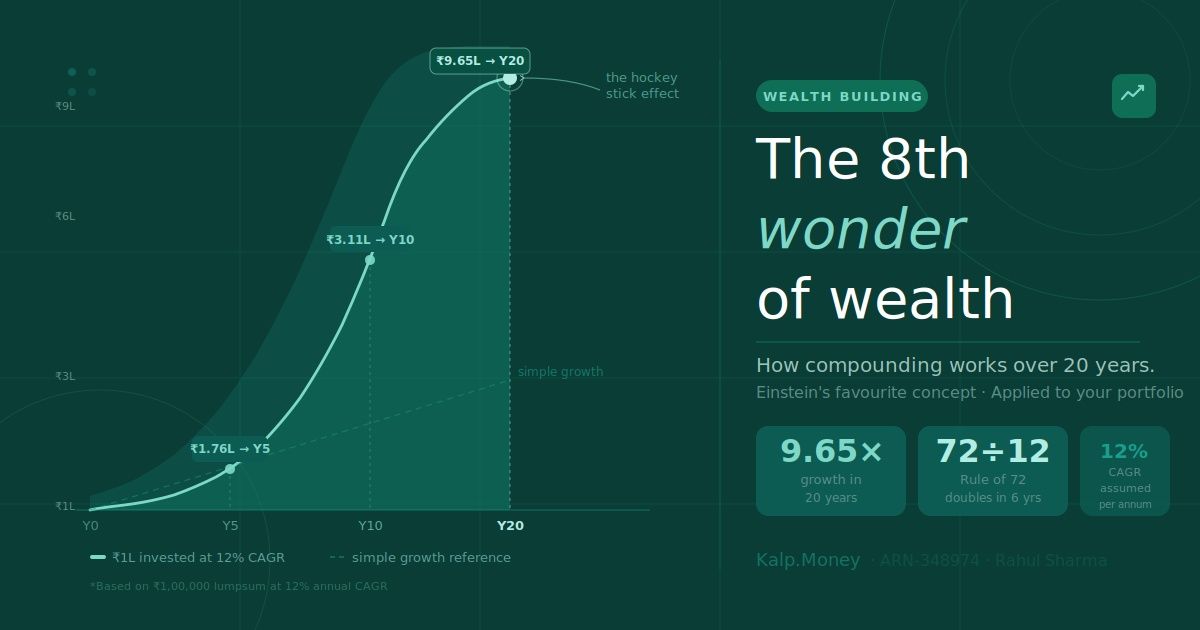

The Rule of 72

A quick mental math trick: divide 72 by your expected annual return to estimate how many years it takes to double your money.

- At 6% (savings account/FD): money doubles every 12 years

- At 9% (conservative equity): money doubles every 8 years

- At 12% (equity SIP average): money doubles every 6 years

🚀 At 12% CAGR, ₹1 Lakh becomes ₹2L (6 yrs) → ₹4L (12 yrs) → ₹8L (18 yrs) → ₹16L (24 yrs). The same money, doing nothing but compounding.

Why time matters more than amount

Priya starts a ₹5,000 SIP at 25. Rahul starts a ₹10,000 SIP at 35. Both retire at 60. At 12% CAGR, Priya ends up with ₹3.2 Crore. Rahul ends up with ₹1.6 Crore — despite investing twice as much per month. The 10-year head start made the difference. This is the power of starting early.

Your action plan

The best time to start was 10 years ago. The second best time is today. Even ₹1,000/month started at 23 will outperform ₹5,000/month started at 40. Don't wait for the perfect fund, the perfect amount, or the perfect market timing. Start, stay consistent, and let mathematics do the heavy lifting.

For your large-cap exposure, always choose a low-cost index fund — the Nifty 50 or Nifty Next 50. The maths are irrefutable: an active manager must beat the market by more than their fee every single year, for 20 years, just to match an index fund. Over 80% fail to do this. Use active funds only in small and mid-cap categories where under-researched companies give skilled managers a real edge. One core index fund + one active mid/small-cap fund. That's the optimal starting structure for most Indian investors.

All content is for educational purposes only. Not SEBI-registered financial advice.

3 Things to Do Today

Take action on what you just learned — right now, before you forget

Check the expense ratio of every fund you own

Log into Zerodha Coin, Groww, or INDmoney right now. Open each fund. Find the TER (Total Expense Ratio). If any large-cap fund charges more than 0.5%, you have a decision to make. Compare it to its benchmark index fund equivalent.

Run the compounding calculator with your own numbers

Go to any SIP calculator. Enter your current monthly investment amount, 12% annual return, and your target years. Now subtract 1% from the return (to simulate higher expense ratio) and see the difference. That difference is real money you may be giving away.

COMPOUNDING CALCULATOR →Research one Nifty 50 index fund for your core portfolio

Look up UTI Nifty 50 Index Fund or Nippon India Index Fund — Nifty Plan. Check their expense ratio (should be under 0.2%). Compare 5-year and 10-year returns against active large-cap funds. Let the data guide your next SIP decision.